Disclaimer: I am not an registered investment advisor and am not compensated either directly or indirectly for any investment advice.

I’ve been an amateur investor for a while now, and what used to only be a personal hobby has slowly turned into a casual, pro-bono consulting service. It all started after I gave a presentation to a class at the end of college encouraging my peers to start investing now (at the beginning of their careers) for retirement rather than waiting a few years (or even a decade). This post has been adapted from a recent email conversation I had with a friend who wanted some advice on how she should go about her first investment.

First off, many friends want to know how they should start thinking about investing. The world of investing can be daunting, so not knowing where to start is enough to leave many on the sidelines. As we’ll see below not thinking about investing at an early age can translate into big differences later in life! This “investment hierarchy of needs” chart details the most widely accepted view of the order of importance with which you should pursue investments. There’s a clear place to start: opening a retirement account.

1. Open either a Regular or Roth 401k (or IRA)

There are two big reasons why, if your employer offers a 401k, it’s by far the best place to start for young, employed investors: taxes and time.

Paying taxes isn’t any fun (for most people), and paying the capital gains tax is even less fun than the money that comes out of your paycheck every other week. That’s because it doesn’t matter who you are, if you make above $33,000 a year, you’ll pay 15% of any capital gains you make (that is if you buy a share of Google at $40 a share and then sell it at $50 a share, you’ll pay $1.50 of the $10 you made in taxes). Given the long-term fiscal outlook of the US, it’s likely that this number will only increase with time. Here’s where a retirement account comes in. The beauty of a retirement account is that it’s protected from the capital gains tax. You can think of these retirement accounts as armored cars, your investments (stocks, bonds, etc.) as the bags of money inside, and any armed thieves are capital gains taxes.

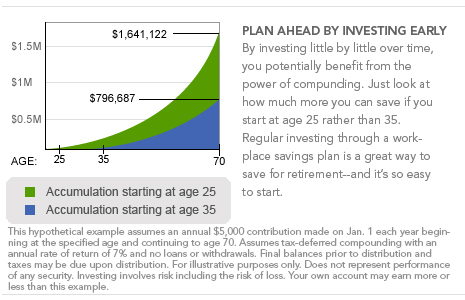

The second reason, time, is just as important. Take a look at the chart below and you’ll see why time (even 2-3 years) can make a huge difference when you get to retirement. The chart takes two scenarios, one person who starts contributing each year at 25 and another who starts at 35. The difference is substantial.

If you’re a young person looking to invest but either a) aren’t employed or b) your employer doesn’t offer a 401k you can always start an IRA, which has a lower annual limit (we’ll get to that later) and no employer match.

So, should you start a Regular or a Roth account? This will depend on your situation. With a Roth account you put post-tax dollars into the account and when drawing the income at retirement it won’t be taxed (neither income tax, nor capital gains tax). With a Regular account you put in pre-tax dollars and when drawing the income out at retirement it will be taxed (income tax, but remember, not capital gains tax). So if you think you’ll be in a higher tax bracket in retirement (either due to increased income or increased taxes, or both) then a Roth account is the way to go. If the opposite, then a Regular account is for you.

2. Invest in a Target Retirement Fund

These types of funds are an amalgamation of several different index funds (funds that track an index of securities) with a very low expense ratios (the amount an investment manager takes out as a fee). I recommend the Vanguard target retirement 2055 fund to most millennials. Vanguard has the lowest expense ratios by far. In addition, target funds will automatically shift its distribution of stocks vs. bonds as you move closer to retirement. For example, the 2055 fund is currently about 90% stocks and 10% bonds, this distribution will slowly start shifting more heavily towards bonds as 2055 gets closer. Stocks are generally more volatile in the short-term, but have a greater return in the long-run than bonds. This is of course assuming that you’re a passive, buy and hold investor who’s looking to be as diversified as possible at the lowest costs.

3. Contribute to your account often and early

As we saw in the graph, this is key! If your employer offers a match, even better! The best way to incentive this is to automatically route a percentage (at least the amount your employer matches, even better if you can put away more) of your paycheck to your account. If you can, put the maximum of $17,500 into your 401k or $5,000 a year into an IRA. One thing that a lot of people don’t know is that you can add to your retirement account for the past year all the way until taxes are due (so you have until April 15, 2014 to contribute towards your 2013 retirement account limit).

If you’ve already gotten all of that taken care of and you’re still hungry for more you can move up to the next level of the hierarchy, opening a brokerage account. I’ll go into some general strategies and guidelines on how to get some exposure to more specific industries or firms using your brokerage account in the next installment. But using the strategies in this post is all most people will need to start saving for retirement effectively.

Comments or questions? Send them to me @jeremysjacob