With companies like King Digital Entertainment, Airbnb, and WhatsApp receiving (or rumored at) valuations of $7 billion, $10 billion and $16 billion respectively it’s hard not to take a trip down memory lane, headed to 15 years ago. Now that we’re living in the age of “the internet of things” and Web 2.0, are we about to live through tech bubble 2.0?

While it may look like some tech companies are in a bubble (it’s hard believe that with Airbnb could be worth more than Hyatt and that King Digital could already be worth double Zynga) there’s one big difference between the current market and the high-flying show that was 1990/2000: earnings.

Back in 1999, it wasn’t unusual for a company with literally zero revenue to go public. Take the classic, ill-fated case of Pets.com. The company went from IPO to liquidation in only 268 days. Irrational exuberance wasn’t just extended to Pets.com and other flash-in-the-pan companies. Cisco was trading at a P/E ratio of 192 in March of 2000. Now Cisco had actual earnings, but not nearly enough to back up that kind of price (its almost impossible for any company to have it). Like all companies, that valuation was given based on the expected earnings of Cisco. Put another way, investors were valuing every $1 in Cisco earnings at $192. That’s just crazy, since even if Cisco tripled its earnings investors would get barely any return on their initial investment.

It looks like this time may actually be different. For example, Google (a large-cap company roughly equivalent to Cisco in 2000) is currently trading at a P/E of about 30. That’s still about double the long-term P/E average of 15, but nowhere near the insanity that was the tech bubble.

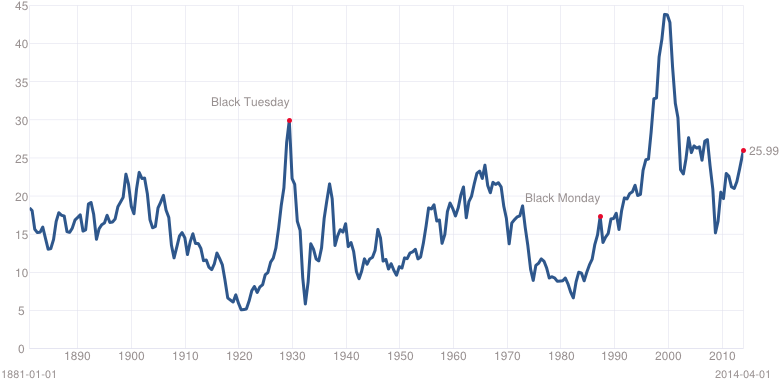

The chart below shows historical data on the Shiller P/E ratio from a great site called mutple, which updates the Shiller P/E and S&P 500 P/E daily. The Shiller P/E uses a broad measure defied as price over 10-year moving averages of earnings, so it isn’t exactly comparable to the P/E ratios for individual companies at any given time. While we aren’t at historical lows by any means we’re also nowhere near the bubble of 1999/2000.

While there are a few companies whose valuations are based more on hype and expectations of enormous profits down the line, the market as a whole is much saner than it was back in 1999. But keep an eye on the these broad P/E measures. If the Shiller P/E Ratio above 35 it means the overall market will have a significantly higher P/E ratio than Black Tuesday and the crash of 1929. But as long as companies keep backing up with valuations with real revenue and GAAP accounting practices we shouldn’t have to worry about having to do any of these things ever again.

Comments or questions? Send them to me @jeremysjacob